21 Jul Q2 2025

The ever-changing tariff dynamic continues to dominate financial headlines. When we sent out our first quarter newsletter on April 4th, equity markets were in a steep decline due to the tariffs announced on “Liberation Day” coming in much higher than expected. The S&P 500 was down about 5% on April 3rd and 6% on April 4th. The downward trend continued until April 9th when the Trump administration issued a 90-day pause on most tariffs until July 9th, which was recently extended until August 1st. The tariff pauses led to a relief rally in equity markets, with the S&P 500 rebounding about 25% off its recent bottom in early April.

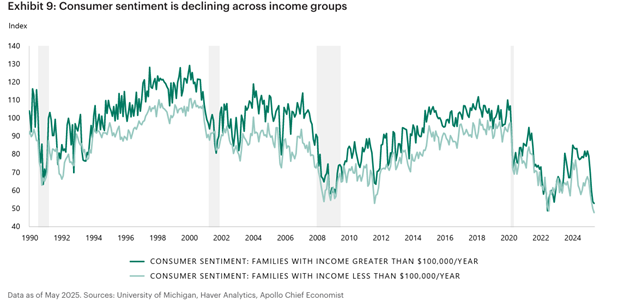

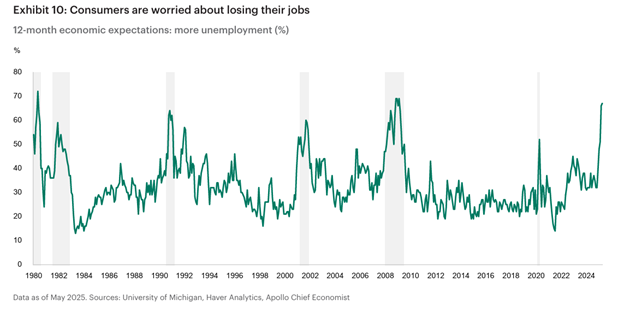

Tariffs are a cost that must be paid by someone or something, and there are three options – foreign suppliers absorb the cost, US companies absorb the cost, or prices to consumers increase. No one knows to what degree foreign and US companies will absorb the cost of tariffs versus how much will pass to the consumer. This uncertainty and the constant changes in tariff rates are hurting consumer and business confidence. Consumer confidence has deteriorated, and people are worried about losing their jobs:

Source: Apollo

Note: The chart above was constructed with data through May. Consumer sentiment ticked up in June and July, but remains at depressed levels.

Source: Apollo

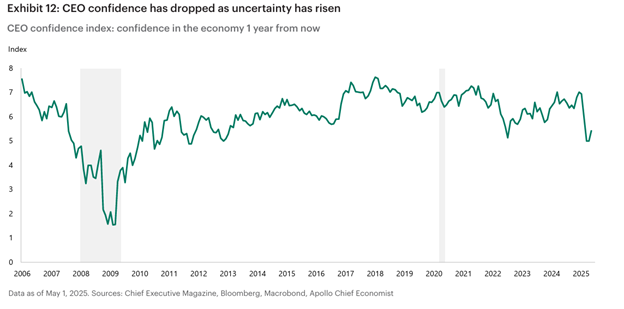

Furthermore, the unpredictable business environment causes companies to pull back on hiring and capital expenditures:

Source: Apollo

The most recent tariff announcements came in the form of letters to foreign governments, each including a tariff rate and a delay until August 1st. The fact that equity markets have not pulled back around these recent tariff announcements can likely be attributed to the belief that announced tariff rates and deadlines will be negotiated down and pushed out. With stocks at extended valuations and a high level of uncertainty around final tariff rates, the short-term risk/reward appears skewed towards a negative surprise.

The other important variable impacted by tariffs is interest rates. The Federal Reserve has held the Fed Funds rate at 4.5% since December. The Fed is widely expected to cut rates later this year, however the uncertain impact of tariffs on inflation has caused the Fed to wait for more data before reducing rates.

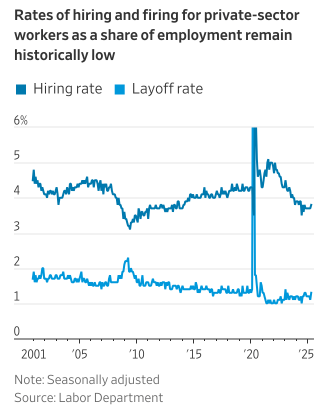

The Fed is stuck in a tough spot. Inflation is measured in various ways, but most indicators peg the annual inflation rate between 2.5% – 3.0%. Headline CPI was released earlier this week, and increased to a higher than expected annual rate of 2.7%. Also, despite the low confidence expressed by consumers and businesses, the economy is currently in solid shape with low unemployment and strong consumer spending. The low unemployment is a result of companies not wanting to fire workers. Hiring is down, but the layoff rate is fairly low:

Source: Wall Street Journal

One final note on the Fed and interest rates. There is current discussion circulating that the Trump administration may try to fire the Fed Chair, Jerome Powell, and replace him with someone more likely to cut interest rates. It is important to note that the Fed Funds rate is set by a vote of the Federal Open Market Committee (FOMC). The Fed Chair does not set the Fed Funds rate, rather the seven members of the Board of Governors of the Federal Reserve System, the President of the Federal Reserve Bank of New York, and four rotating Federal Reserve Bank presidents collectively vote on the Fed Funds rate.

I expect volatility to continue in the second half of the year. Long-time market strategist Ed Yardeni recently said, “In my career, I don’t recall so much uncertainty in such a short period of time.” Uncertainty can cause fluctuations and be frustrating in the short term, but it provides opportunities and can lead to strong compounding returns over the long term. As we enter the second quarter earnings season, we expect to hear how companies are dealing with the prevailing uncertainty.

Please see below for portfolio commentary and activity.

Core Equity

Top performing stocks during the quarter included Broadcom, Quanta Services, Nvidia, Ciena, Microsoft, and Eaton. Laggards included Iqvia, Schlumberger, Thermo Fisher Scientific, and NXP Semiconductors. Walmart was one of three new companies added to the portfolio during the quarter. Over the last decade Walmart has deployed approximately $200b in capital expenditures focused on fundamentally modernizing operations including supply chain efficiency, optimizing inventory management systems, refining purchasing decisions through data analytics, and significantly improving the overall customer experience, both in-store and online. This level of spending is approximately twice the amount spent by Home Depot, Lowe’s, Costco, and Target combined during the same period. We believe Walmart is now at an inflection point, ready to harvest the returns from these extensive upgrades. A recap of trades during the quarter:

- New position: Broadcom, Walmart, S&P Global

- Increased position size: Thermo Fisher Scientific, Zebra Technologies

- Exited positions: NXP Semiconductors, Iqvia, AES Corp

- Decreased position size: Bank of America, JPMorgan Chase

Covered Call

On average, five to six options expire each month in our Covered Call portfolio. If the option expires worthless, we typically sell another option on the same stock. If the stock price is above the option strike, and the underlying stock is called away, we typically replace the holding with a new covered call position. Trading activity during the quarter:

- New positions: Oracle, Citigroup, Carrier

- Option rewrites: Apple, Comcast, Qualcomm, TJX Companies, Morgan Stanley, Union Pacific, Applied Materials, US Bancorp, Nike, Merck, Electronic Arts, Sysco, Zimmer Biomet, ConocoPhillips, Becton Dickinson

- Positions called away: Tyson Foods, Microchip Technology

- Positions sold: Dow

Diversified Income

Top performing positions during the quarter included State Street, IBM, Whirlpool, and Cisco. Laggards included Bristol-Myers Squibb, LyondellBasell, and Chevron. Trading activity during the quarter:

- New positions: Allstate preferred Series H

- Increase position size: Target, United Parcel Service, Bristol-Myers Squibb, Pfizer

- Exited positions: Short-term Treasury ETF

Tom Searson, CFA

The analysis and performance information contained herein reflects that of portfolios used by Providence Capital Advisors, LLC, a Securities and Exchange Commission Registered Investment Advisor. This information should not be relied upon for tax purposes and is based upon sources believed to be reliable. No guarantee is made to the completeness or accuracy of this information. Providence Capital Advisors, LLC shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions contained herein or their use, which do not constitute investment advice, are provided as of the date written, are provided solely for informational purposes, and therefore are not an offer to buy or sell a security. This information has not been tailored to suit any individual.

Providence Capital Advisors, LLC does not guarantee the results of its advice or recommendations, or that the objectives of a strategy will be achieved. Portfolios offered by Providence Capital Advisors, LLC may not have contained and/or may not currently contain the same underlying holdings and may have been and/or may currently be managed according to rules or restrictions established by Providence Capital Advisors, LLC. The income numbers for Covered Call and Diversified Income are based on one portfolio in the composite that serves as the model portfolio. Actual income returns may be different for other portfolios. Employees of Providence Capital Advisors, LLC may have holdings in the securities and/or utilize the same portfolio strategies as presented herein.

Benchmark returns are used for comparative purposes only and are not intended to directly parallel the risk or investment style of the accounts included in our investments. The volatility of the indices compared herein may be materially different from that of the compared Providence Capital Advisors, LLC strategy. There is no guarantee that the strategies will outperform, or even match, benchmark returns over the long term.

This commentary contains certain forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason.

Past performance is not indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended or undertaken by Providence Capital Advisors, LLC) will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the payment of which would have the effect of decreasing historical performance results.