17 May November 2017 – The Long, Steady Grind

The Long, Steady Grind

2017 has been a strong year in the equity markets, however the lack of volatility has been both surprising and abnormal. According to data provided by Bespoke Investment Group, the S&P 500 is now in the longest uptrend on record without even a modest 3% pullback. Combing through data provided by JPMorgan depicts the same lack of volatility in a different light. Looking back at returns of the S&P 500 since 1980, the average intra-year decline is 14.1%. This year it is less than 3%, which is the lowest intra-year pullback in that data set.

Despite this lack of volatility, the market is not overcome with euphoria. The enthusiasm that led to major asset bubbles such as technology stocks during the late 1990s or U.S. housing prices in 2006/2007 doesn’t seem to permeate the markets. I’m not going to step into the debate over whether cryptocurrencies are in a bubble, but Bitcoin bulls may want to overlay a chart of Bitcoin with Dutch tulip bulbs in the 1600s. One other area of potential “Irrational Exuberance” may be in Argentina’s ability to issue a 100 year bond earlier this year. Argentina has defaulted 6 times in the last 100 years including most recently in 2014. These examples of potential euphoria are more niche-based, and I would argue that while asset values certainly aren’t cheap, most do not seem excessively valued either.

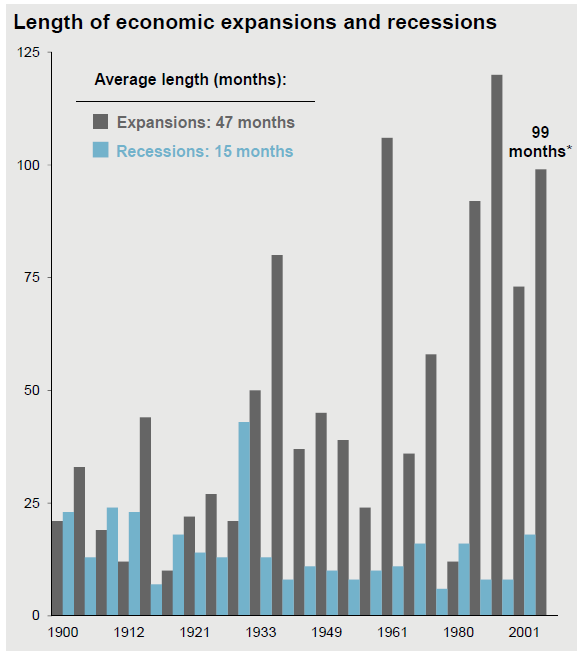

Switching gears slightly to the economy, we are now in the 3rd longest economic expansion on record:

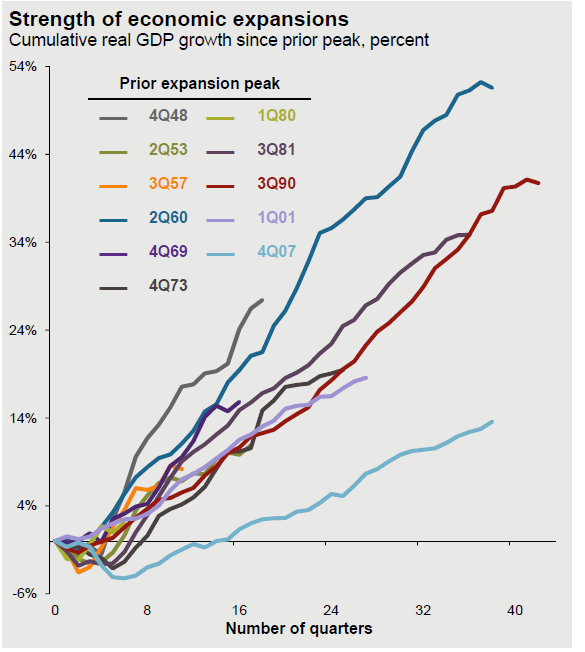

The sheer length of the expansion causes some consternation about the timing of the next recession, however the next chart is an important variable to consider. While undoubtedly long in nature, the current economic expansion pales in comparison to previous expansions in cumulative economic growth.

So how do we invest in this type of market? Volatility is extremely low and likely to increase at some point. Valuations are not cheap, but generally not excessive either. Economic data does not indicate that a recession is on the immediate horizon, but we are highly likely closer to the end of the cycle than the beginning.

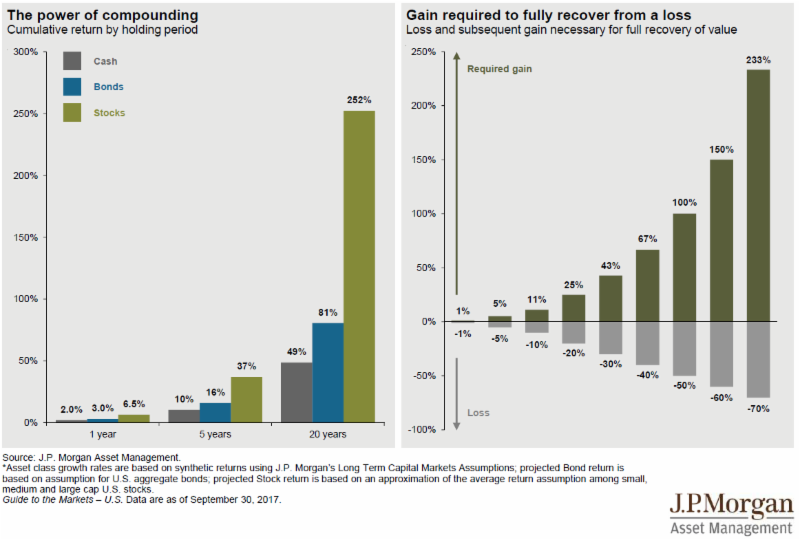

The next 2 charts show the tightrope we walk in investing that seems amplified during the current environment. The chart on the left shows the power of compounding or what Albert Einstein called, “the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.” The translation of this chart is the importance of staying invested through market cycles. The chart on the right shows the mathematical importance of protecting downside risk: a 20% loss of principal necessitates a 25% return to get back to even.

Balancing all of these variables leaves two important conclusions, in my opinion. First, know what you own. While it is certainly always important to know what you own, the underlying fundamentals of a company are more important late in the business cycle while investors are arguably more complacent than early in the business cycle while investors are still nervous. In other words, a rising tide lifts all boats, but things get exposed when the tide pulls back. Secondly, I think it is important to have a cash allocation across our investment strategies. This cash allocation is both a strategic decision to provide dry powder ready to deploy when volatility returns and also a result of the difficulty in finding new investment opportunities as valuations continue to creep higher. Our cash levels will change as we find new investment opportunities and challenge our existing holdings, and we will stay ready to take advantage of opportunities that present themselves in market pullbacks that will inevitably occur.

Happy Thanksgiving from Providence Capital Advisors!

Tom Searson, CFA