17 May May 2018 – Inversion

Inversion

At the end of this month we will pass an economic milestone. Since the trough in June 2009, the US economy will have expanded for 107 consecutive months when we move from May into June. This will make the current expansion the second longest on record, surpassed only by the expansion from March 1991 to March 2001. If the economy can continue to expand until July 2019, we will have a new record for the longest economic expansion in the United States.

Given the duration of our current expansion, it is highly likely that we are closer to the end of this business cycle than the beginning. As such, investors are continuously looking for clues as to when the economy will pull back into a recession. There have been 10 bear markets (defined as a 20% or greater drop in the stock market) dating back to 1929, and 8 of those 10 have been associated with a recession. This link between recessions and bear markets keeps investors on the constant lookout for an economic downturn.

One signal watched closely by investors and economists (and often cited in the press) is what is referred to as an inverted yield curve. Bonds with a longer maturity typically have higher interest rates than bonds with a shorter maturity. For example, an investor willing to commit money to a 10 year US Treasury bond is usually rewarded with a higher interest rate than an investor only willing to commit to a 2 year US treasury bond. The greater the difference between the higher long-term rates and the lower short-term rates, the “steeper” the yield curve. As the difference between those rates narrows the yield curve is “flattening” and when short-term rates are higher than long-term rates the curve becomes “inverted”.

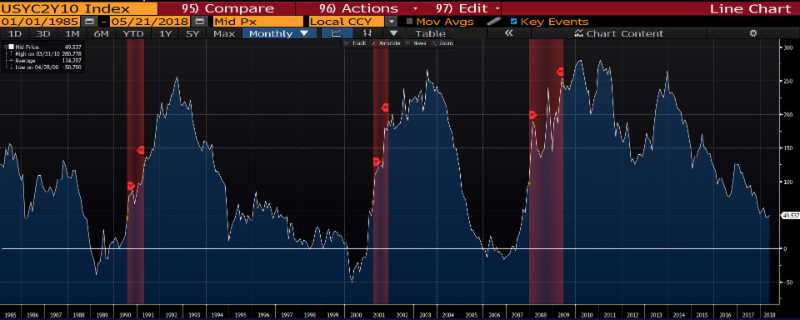

One of the main reasons yield curve inversions are closely followed is that the yield curve has inverted before every recession since the late 1950s. The chart below depicts the spread between 2 and 10 year US Treasuries overlaid against recessions (shaded red areas). The white horizontal line is the point of an exactly flat yield curve. As you can see, this spread appears to be an important signal of an upcoming recession. As you can also see, the yield curve is at its flattest point since 2007…..

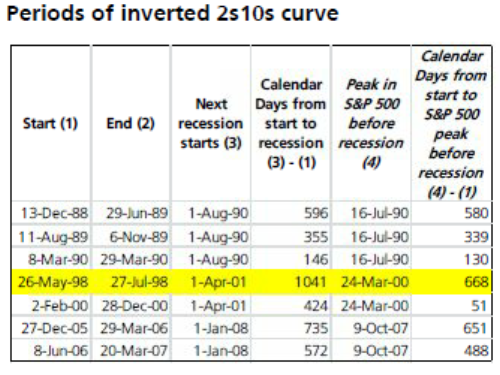

Digging the next level deeper reveals a much more complicated scenario for investors. We are still a good bit away from the yield curve inverting, but if it does, how long until the beginning of the next recession? And more importantly, how long until the stock market peaks? The data in table below shows the difficulty in using an inverted yield curve as an investment tool. In one instance the S&P 500 peaked only 51 days after the yield curve inverted. In another instance, the market peaked 668 days later. So using these instances as barometers, the market could peak anywhere from less than 2 months to almost 2 years after the yield curve inverts. Somewhat helpful, but clearly a very wide range.

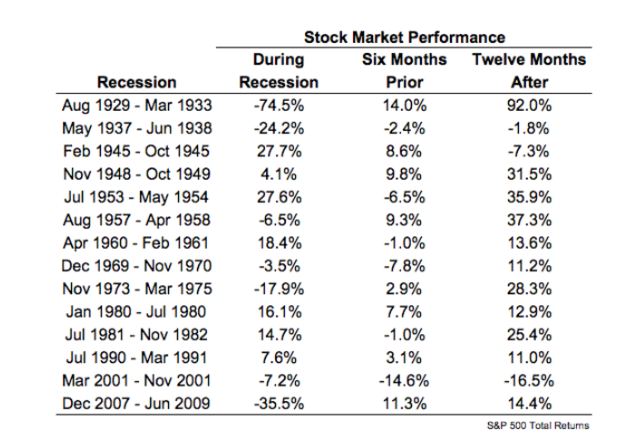

Even if someone was able to time an upcoming recession, how should this impact their investment decision making? The table below shows S&P 500 returns during, six months prior, and twelve months after every recession since the onset of the Great Depression.

Looking at the table above, stock market returns have actually been positive during 7 of the last 14 recessions. The stock market is a forward-looking mechanism, so one might think that the negative returns always take place before the recession. Unfortunately the data does not provide clarity here either. Stock market returns have been positive for the 6 months prior to the recession in 8 of the last 14 recessions.

If the yield curve continues to flatten you will likely hear prognosticators pounding the table that a recession is near. In one sense they are right, if the yield curve inverts it is likely that a recession is on the horizon. But answering questions like when and what does that mean for stock market returns are much more complex. In the end, this speaks to the importance of balance and managing through cycles rather than trying to time them. So while we certainly incorporate macroeconomic factors into our investment decision making process, we allocate more focus to identifying companies that can succeed in different economic climates. We also have cash on hand across our investment portfolios, ready to put to work in the event of market volatility.

Tom Searson, CFA