19 May February 2020 – Coronavirus Fears

Coronavirus (COVID-19) fears have dominated news headlines and gripped global financial markets with fear.

Once seemingly contained to China, the virus has spread globally and now is present in every continent except for Antarctica. The first case in the United States of unknown origin was recently confirmed. The broad consensus now is that it is only a matter of time before there are increasing confirmed cases in the U.S.

While concerns about the virus both from a health standpoint and from its impact on the economy are quite real and significant, there are a few things to consider as the market has begun to reprice in acknowledgment of these risks.

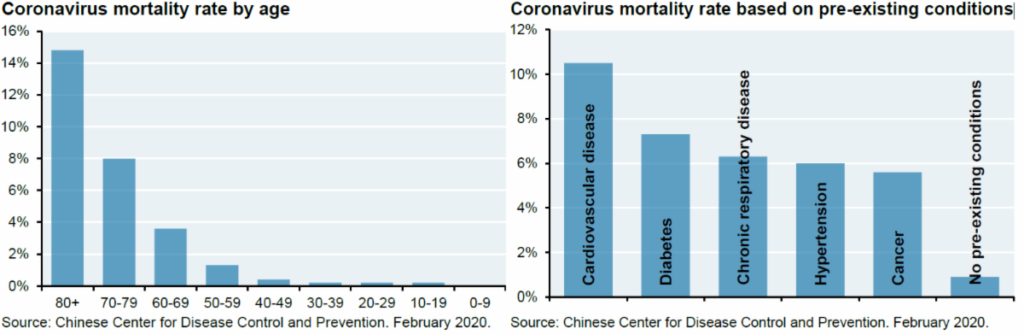

Mortality rates seem to be very closely tied to age and pre-existing conditions. We encourage readers to focus on relative, rather than absolute, mortality rates when reviewing the charts below or any other current data about the virus. Mortality rates tend to be overestimated at this stage of an epidemic because the denominator of the calculation (# of people infected) tends to be underestimated more than the numerator (# of deaths) is likely to increase.

Also, in comparing the Coronavirus to Influenza, the US Centers for Disease Control estimates that from October 1, 2019 through February 15, 2020 there have been 29 million to 41 million flu illnesses and 16,000 to 41,000 flu-related deaths. So far, these numbers dwarf the cases of Coronavirus across the entire globe. While it appears that the risks of the Coronavirus are considerably more serious than the flu, media coverage and markets may overreact in embracing dire prognostications.

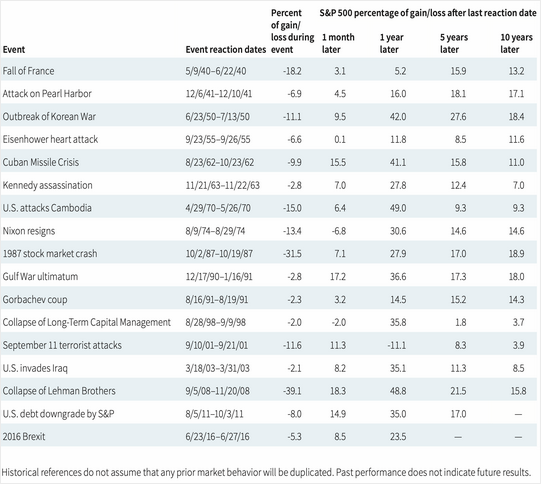

No one knows how far and fast the Coronavirus will spread and what the economic impact will be, and this uncertainty is driving the recent, violent market movements. Although the pain may feel palpable now, event-driven market declines are historically followed by relatively quick recoveries, as you can see in the table below.

Expanding this list to include epidemics such as SARS, MERS, and Ebola provides a similar result. Over time, viruses tend to get contained and investors return to focusing on growth fundamentals.

It may seem tempting to want to sell now and wait for the virus to be contained before getting back in to the markets. Unfortunately waiting until the environment looks good will likely cause investors to miss out on significant gains. Markets are forward-looking, and will rebound prior to fundamentals bottoming, reinforcing that trying to time the markets is a futile exercise. We build our clients’ asset allocations to navigate through times like this. We have navigated through tough times in the past, and we certainly will again in the future.

We used the strong returns last year to build significant cash balances across our investment portfolios. Prior to this pullback stocks were at all-time highs with arguably stretched valuations. Although we cannot claim to have anticipated the cause, we were prepared for a pullback from the previous lofty levels. We are now beginning to slowly invest some of the cash in the portfolios in what we believe are solid, long-term opportunities. And if the markets continue their downward trajectory, we have plenty of cash remaining to invest in other opportunities that present themselves.

Tom Searson, CFA