17 May February 2018 – Tax Newsletter

Tax season is in full swing, and while most clients are still pulling together 2017 documents for their preparer, several have already started wondering, “What will happen to my tax situation in 2018?” There is a perception that the new law lowers taxes and simplifies the tax preparation process, and while that may be true for some taxpayers, it creates significant strategic opportunities for others. At Providence Capital Advisors we are prepared for planning in the new tax landscape and have included below changes implemented by the new Tax Cuts & Job Act (hereinafter the Act) that may impact you.

Several of the new provisions outlined below take effect in 2018 and sunset after December 31, 2025, and while many need additional regulatory explanation, the following is a selection of the most significant changes for individual taxpayers.

Tax rate changes – Tax rates are reduced by 1-2% in all but the lowest bracket, which will remain constant at 10%. Taxpayers subject to the highest marginal rate will see their rate drop from 39.6% to 37%. Additionally the new brackets are wider, meaning it takes significantly more income to be in the top bracket than under the previous law. For example, a married couple filing a joint return for 2018 will enter the highest bracket once taxable income exceeds $600,000, whereas for 2017, the same tax payers are subject to the highest bracket when taxable income exceeds $470,701.

Capital Gains – Under previous law, capital gain and qualified dividend rates were tied to tax brackets. The Act eliminates the link to tax brackets and applies the preferential capital gains rate based on taxable income.

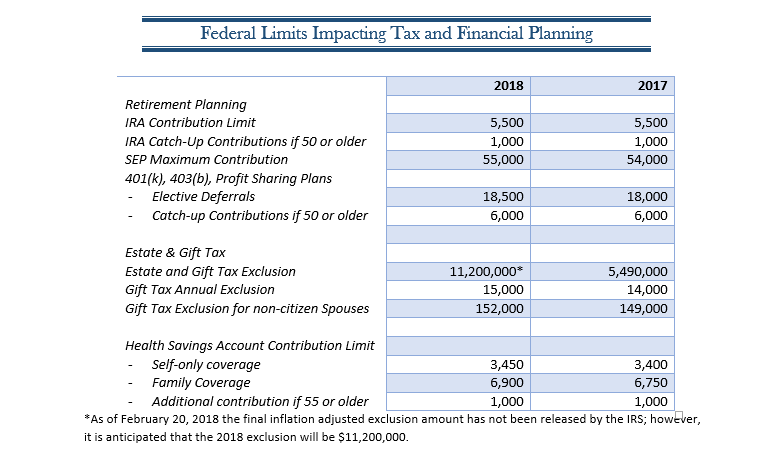

Additional Medicare Tax & Net Investment Income Tax (NIIT) – No change to the .9% additional Medicare tax on wages and self-employment income in excess of $250,000 (Married Filing Joint “MFJ”) or $200,000 (Single). The 3.8% NIIT also remains unchanged and applies to taxpayers with net investment income and modified adjusted gross income greater than $250,000 (MFJ) or $200,000 (Single).

Alternative Minimum Tax – The Alternative Minimum Tax remains in place for tax years 2018 – 2025, but due to the increased exemption and phase-out amounts coupled with limitations on itemized deductions, it is anticipated that fewer individuals will be subject to AMT.

Kiddie Tax – Although most individuals will benefit from wider brackets and reduced rates, those subject to the kiddie tax could receive an unwelcome surprise when completing 2018 income tax returns. Under the prior law dependents with unearned income subject to the kiddie tax were taxed at their parent’s rate; however, under the Act a child’s unearned income is subject to the trust and estate tax schedule where income in excess of $12,500 is taxed at 37%.

Increased Standard Deduction and Limitations on popular Itemized deductions – The deduction for personal exemptions is repealed for tax years beginning after 2017 and before 2026. However, the standard deduction is increased to $12,000 for single filers, $18,000 for heads of household and $24,000 for joint returns. The Act retains the additional deduction for those over 65 and/or blind ($1,300 for joint filers, $1,600 for others). For those who benefit from itemizing, the Act repeals the Pease Limitation, which reduced total itemized deductions for taxpayers whose AGI exceeds certain thresholds and adjusts other itemized deductions as follows:

- Medical Expenses – Unlike other deductions which were reduced or restricted, the medical expense deduction is expanded under the Act. For tax years 2017 and 2018, the AGI threshold for medical expenses drops to 7.5% from 10%. The threshold will revert back to pre-Act levels beginning in 2019.

- Mortgage Interest – Existing mortgages are not impacted by the Act; therefore, interest on debt up to $1 million remains deductible. Under the Act, interest on acquisition indebtedness is limited for mortgages incurred after December 15, 2017 to debt of $750,000 and applies to primary and second homes where the debt was used to purchase, construct or improve the home. The new limitation sunsets for tax years beginning after 2025 and reverts to $1 million. The Act also eliminates the deduction for home equity indebtedness for tax years beginning after 2017 and before 2026.

- State and Local Taxes – The Act caps the deduction for personal property, real estate, and state income taxes to $10,000 in aggregate.

- Charitable Planning – The deduction for charitable contributions remains intact under the Act, and the AGI limitation for cash contributions to public charity increases from 50% to 60%. However, the 80% deduction previously allowed for contributions to colleges and universities where the taxpayer receives a right to purchase tickets is eliminated.

- Miscellaneous Itemized Deductions – For tax years beginning after 2017 and before 2026, the Act repeals all miscellaneous itemized deductions which includes unreimbursed business expenses and professional fees.

20% Deduction for Qualifying Income – This provision creates a significant deduction for business owners and promises to be the most complex. The deduction was created as a means to bridge the gap between the highest corporate and individual rates, 21% and 37% respectively. In short, the provision offers a 20% deduction to non-corporate taxpayers to offset qualified business income, qualified REIT dividends, qualified cooperative dividends, and income from a publically traded partnership that is not treated as a corporation. For qualified business income, the deduction is limited or eliminated entirely for service providers in certain industries or taxpayers whose taxable income exceeds $315,000. This provision is set to expire for tax years beginning after 2025.

529 Expansion – Under the Act, the definition of qualified higher education expenses is expanded to include tuition paid for private/religious elementary and secondary education, up to $10,000 per student, per tax year. It remains unclear if states will adopt the new expanded federal definition of qualified higher education expenses.

Roth Recharacterizations – The Act repeals the provision permitting taxpayers to recharacterize or unwind a conversion from a Traditional IRA to Roth IRA. Taxpayers are still permitted to make “back door” Roth contributions where AGI limits prevent contribution directly to Roth IRAs.

While this list is not all-inclusive, it touches on many of the provisions that will impact individual taxpayers. From the limitations on itemized deductions to the small business deduction, Providence Capital Advisors is equipped to assist clients in identifying strategic planning opportunities arising as a result of the Tax Cut & Jobs Act.

Providence Capital Advisors is a SEC Registered Investment Advisor and not a CPA firm. The tax information provided is general and educational in nature, and should not be construed as legal or tax advice. Information provided relates to taxation at the federal level only. Always consult an attorney or tax professional regarding your specific situation.

Melissa Wall, CFP, CPA