08 May December 2015 – Turning Point for Wage Growth

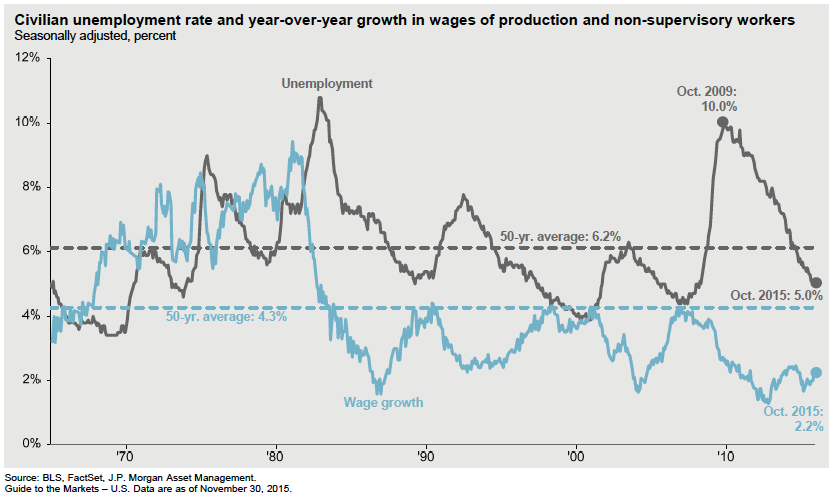

Since the end of the Great Recession in 2009 the unemployment rate has decreased from 10.0% to 5.0%, and over 13 million net jobs have been created. As the chart below shows, wage growth historically increases as the unemployment rate decreases. This economic principle has remained absent in the present recovery.

One reason for the lack of wage growth is that the 5.0% headline unemployment number understates the true employment backdrop. Economists describe the labor environment as having “slack” which suppresses wage growth. This slack can be seen when broadening the unemployment rate definition to include people not in the labor force who want work but have not searched for a job in the last 4 weeks and those that are employed part time for economic reasons, a statistic referred to as U-6. U-6 unemployment has dropped from 17.1% to 9.9% over the last 6 years, but is still above the 8.0% level reached in 2006 and the 7.0% level reaching in 2000. Slack in the labor market can also be seen by inspecting the labor force participation rate, which now stands at 62.5%. This rate has declined sharply since 2008 for both demographic and economic reasons, and now sits at a level last seen in the late 1970s. Simply put, wage growth likely would have been stronger in 2015 if U-6 unemployment was closer to headline unemployment, as it was in previous recoveries.

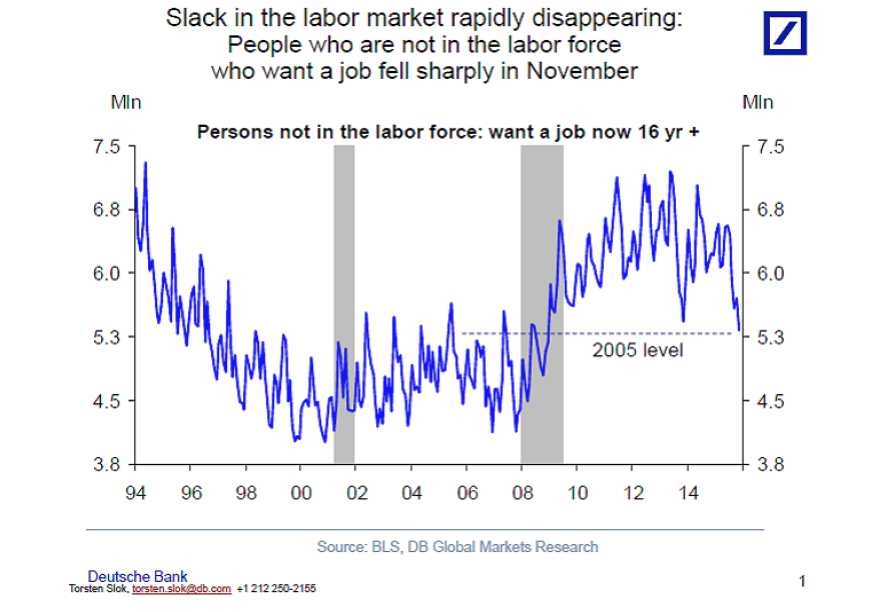

Despite persistent slack in the labor force throughout 2015, signs of tightening are beginning to appear.

In addition to the chart above that shows a decrease in the number of people not in the labor force who want a job, other data is beginning to show tightening:

- Number of people per job opening is back to 2006-2007 levels

- Number of unemployed workers per job opening is approaching 1, after peaking above 6 in 2009

- Number of people voluntarily quitting their job has increased significantly since bottoming in 2010

This tightening of the labor force is likely to lead to wage gains, which have proved elusive throughout the current recovery. Anecdotally we have started to see this as companies such as Walmart, Target, McDonalds, Ford, and General Motors have all announced pay raises.

Looking into 2016, employment growth may slow from the 2015 pace of 210,000 jobs created each month, but I think wage gains will finally start to accelerate. One disappointing hallmark of this economic recovery has been its frustratingly slow pace. I think this slow and steady pace will be seen in 2016, as wage growth increases from its current level, but accelerates slowly.

A long list of other variables will affect 2016 stock market returns including the pace of interest rate increases by the Fed, the smoothness of China’s continued shift to a consumer-driven economy, commodity price movements, actions by other central banks around the globe, the strength of the U.S. Dollar, and many others. The current bull market is the third longest on record. Although bull markets don’t die solely of old age, strong upside is likely limited in 2016. I think the highest probability is that stock market returns in 2016 are similar to earnings growth for the year, likely mid-single digits. However, I believe volatility is likely to increase next year as the market digests changes in the variables listed above. This increased volatility widens the range of potential stock market returns during the year and increases the importance of being nimble in evaluating investment opportunities.