17 May August 2019 – A New Record and a Rate Cut

As we turned the calendar to August, the current economic expansion in the United States officially became the longest expansion on record, surpassing the 10 year expansion of the 1990s. That expansion ended with the bursting of the tech bubble when nonsensical valuations were placed on companies that were exposed to the internet, networking, or telecommunications. While there are certainly areas of the markets that appear expensive, I do not see the overall exuberance and valuation extremes that permeated the late 1990s.

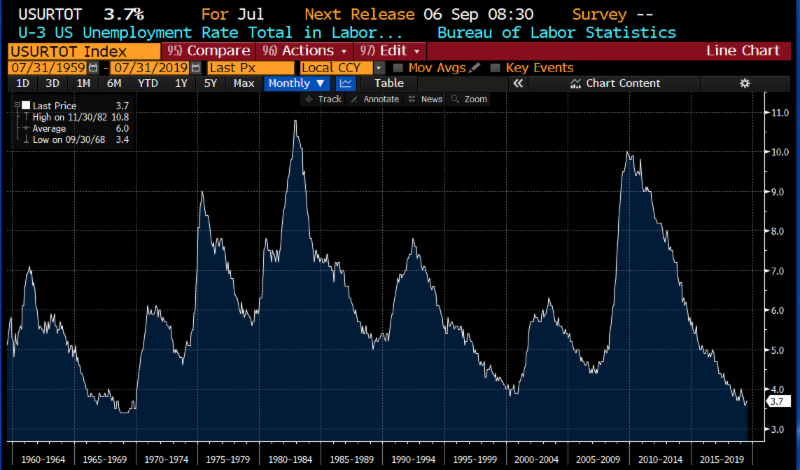

As a result of this long expansion, U.S. households are on solid economic footing. The current unemployment rate of 3.7% marks the 17th month in a row that unemployment has been 4.0% or less. We have not seen this level of sustained, low unemployment since the late 1960s.

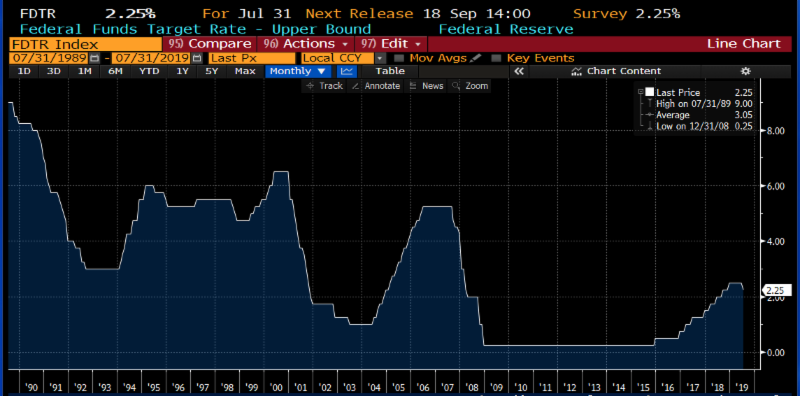

Despite this historic economic milestone, seemingly solid backdrop, and strong stock and bond returns this year, few glasses of champagne are being lifted in celebration. In fact, the Federal Reserve lowered the federal funds rate by 0.25% last week, the first interest rate cut since 2008.

The Fed typically lowers rates during a recession in an effort to help spur growth. This rate cut was, “intended to insure against downside risks from weak global growth and trade policy uncertainty; to help offset the effects these factors are currently having on the economy; and to promote a faster return of inflation to our symmetric 2 percent objective.” In other words, the U.S. economy is on solid footing, but the Fed is worried about slower growth internationally and uncertainty arising from trade negotiations and tariffs. Low inflation gives the Fed cover to cut rates in an effort to boost economic activity.

The Fed is trying to sustain the expansion by preemptively cutting rates as insurance against trade uncertainty and slow global growth spilling over to negatively impact U.S. growth. Despite the Fed’s efforts, trade uncertainty is the largest issue facing global markets, and interest rate cuts are unlikely to provide enough cushion to offset those uncertainties. Fed Chairman Jerome Powell admitted during his press conference announcing the rate cut that, “there isn’t a lot of experience in responding to global trade tensions.” Business leaders are cautious to invest during times of uncertainty because many decisions have a multi-year horizon. Chairman Powell noted some concern with the effects of the uncertainty saying, “manufacturing output has declined for two consecutive quarters, and business fixed investment fell in the second quarter.”

Global growth is slowing, and we are hearing from corporate management teams that the trade dispute between the U.S. and China is magnifying the slowdown. Stock market volatility will likely continue as investors debate whether a recession is around the corner or the economic expansion continues.

We have used the strong stock returns this year to increase the cash weighting and defensive positioning of our portfolios. The calendar turn to August not only marked the longest economic expansion in U.S. history, the first few days of the month also included a return of volatility. As always, we will look to use times of volatility to deploy some of the cash that has accumulated in the portfolios as attractive investment opportunities arise.

Tom Searson, CFA