07 Apr Q1 2025

After two consecutive strong years in equity markets, volatility is rearing its ugly head, and tariffs are the focus. The significant increase in tariffs announced Wednesday evening is sparking valid concerns of slowing growth and increasing inflation.

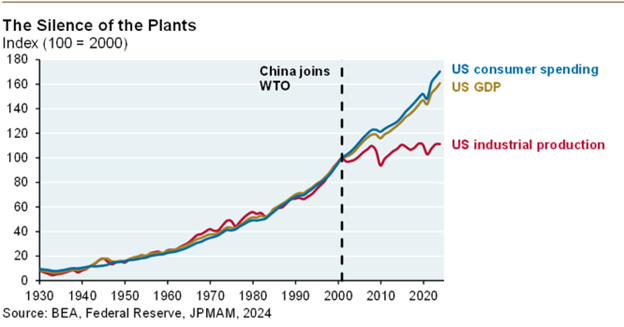

I thought it would be helpful to start this newsletter by discussing the primary problem the administration is attempting to address. As seen in the chart below, consumer spending, GDP, and industrial production in the United States closely tracked each other from 1930 -2000. When China joined the World Trade Organization in 2000, industrial production flatlined while consumer spending and GDP continued to move upward in lockstep.

Source: JP Morgan Chase

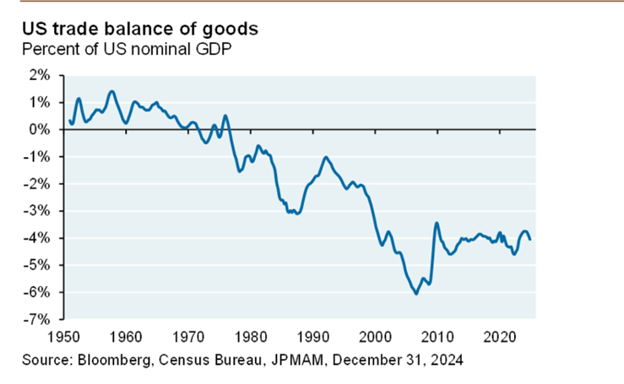

Translating into plain English, US consumers continued spending and economic growth continued, but we stopped making stuff. This resulted in a large trade deficit as measured in goods:

Source: JP Morgan Chase

The last twenty-five years have been a favorable time for consumers, companies, and investors. The overall price of goods remained fairly flat from 2000 until Covid hit in 2020, giving consumers access to cheap goods. Companies benefited from both cheap input costs and cheap labor from a global supply chain, and the benefits to companies flowed through to investors. The downside to this boon is that domestic jobs for industrial production dried up, leading to negative impacts on many families and communities. In addition, global supply chains can leave countries vulnerable to depend on unfriendly regimes for critical needs.

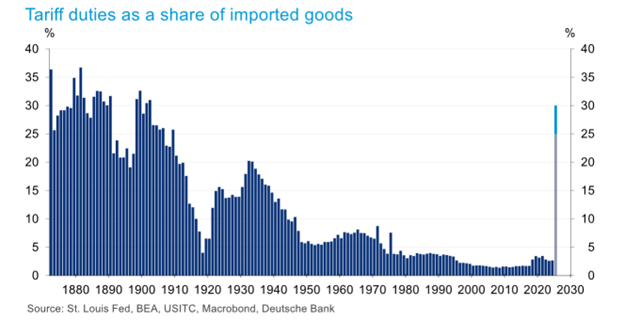

The administration has indicated that they are attempting to reshore domestic manufacturing and lower the deficit through the use of tariffs. Economists have disagreed with this approach highlighting that they believe this will slow growth and increase inflation. Although the market anticipated an increase in tariffs, Wednesday evening’s announcement was broader and more severe than expected. Tariffs as a share of imported goods are now at the highest level in over 100 years:

Source: Deutsche Bank

Company management teams are scrambling to try to predict the future landscape. Will other countries retaliate with more tariffs, and, if so, what does that look like? Conversely, are the recently announced tariffs a high-water mark that will be negotiated down country by country? Building new manufacturing is a costly and time-intensive process, and companies cannot simply flip a switch and undo global supply chains that have been developing since the end of World War II. Furthermore, even if companies do increase domestic production, they must find trained workers and a supply chain that can fulfill input needs. Reengineering the global supply chain is a complex problem that will not be resolved easily or quickly. It is prudent to expect more volatility as company management teams and investors grapple with an ever-changing environment.

In a time of uncertainty, I think it is important to revisit two critical components of disciplined investment management – appropriate asset allocation and the inability to time markets.

Appropriate asset allocation is critical. Equity markets posted a negative quarterly return for the first time since 2022. Despite this negative backdrop, balanced and conservative investors held in relatively well during the quarter. Bonds and high-dividend stocks both posted positive returns. Growth investments generally posted negative returns during the quarter, but investors that are slanted towards growth should have a long-term investment horizon, leaving time for recovery. Another way to think about pullbacks in equity markets is that short-term negative returns are the price that investors pay for long-term investment success.

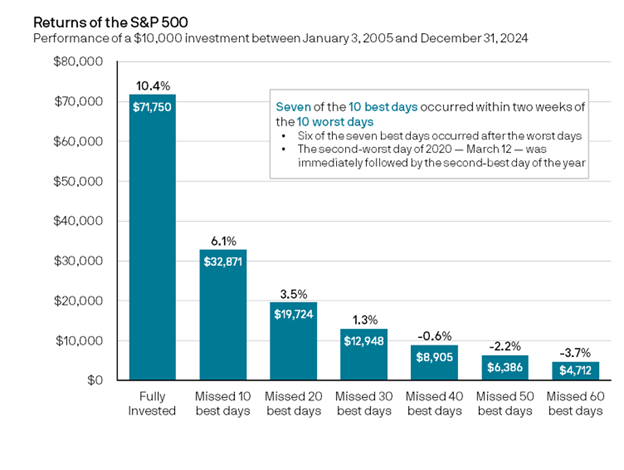

Yesterday was the worst day in the stock market since 2020, and the downturn may certainly continue. It is painful to be invested on days like yesterday, and everyone would like to avoid being invested during a pullback. Unfortunately it is not possible to participate in the upside of investing in equities without exposure to the downside. On that note, I find the information in the chart below absolutely staggering. If someone invested $10,000 in the S&P 500 beginning in 2005 and kept it fully invested for the next 20 years, the investor would have over $71,000. If, during these same 20 years, the investor missed out on only the 10 best days, the original investment would now be worth about $32,000, or less than half of a portfolio that stayed fully invested. Missing out on the 20 best days (averaging only 1 day per year!) cuts the investment return to under $20,000.

Source: JP Morgan Chase

Importantly, as shown in the chart, seven of the ten best days during that period occurred within two weeks of the ten worst days. This means that those days that are so critical to long-term success take place during the toughest times in the market. Those who try to time the market typically get whipsawed and end up with sub-optimal returns.

Please see below for portfolio commentary and trading activity during the quarter.

Core Equity

Top performing stocks during the quarter included Roche, Abbott Labs, Linde, and Deere. Laggards during the quarter were Ciena, Zebra Technologies, Chart Industries, and Nvidia. We initiated a new position in Quanta Services during the quarter. Quanta provides construction services, with a primary focus on electrical transmission and distribution. We believe the combination of the necessary investment to the aging electrical grid in the United States and an upward inflection of power demand for electrification and data center needs sets up Quanta for strong future growth. A recap of trades during the quarter:

- New position: Quanta Services

- Exited positions: Advanced Micro Devices, Aptiv, Booz Allen Hamilton

Covered Call

On average, five to six options expire each month in our Covered Call portfolio. If the option expires worthless, we typically sell another option on the same stock. If the stock price is above the option strike, and the underlying stock is called away, we typically replace the holding with a new covered call position. Trading activity during the quarter:

- New positions: Apple, TJX Companies, Morgan Stanley

- Option rewrites: ConocoPhillips, Dow, Qualcomm, Tyson Foods, Comcast, Microchip, Nike, Union Pacific, Sysco, Applied Materials, Merck, US Bancorp, Becton Dickinson, Electronic Arts, Zimmer Biomet, Hewlett Packard Enterprise

- Positions called away: Citigroup, Emerson Electric

Diversified Income

Top performing positions during the quarter included AT&T, American Electric Power, Abbvie, and Novartis. Laggards included Target, Whirlpool, UPS, and US Bancorp. Trading activity during the quarter:

- New positions: State Street

- Increase position size: General Mills

- Decreased position size: IBM, AT&T, Cisco

Tom Searson, CFA

The analysis and performance information contained herein reflects that of portfolios used by Providence Capital Advisors, LLC, a Securities and Exchange Commission Registered Investment Advisor. This information should not be relied upon for tax purposes and is based upon sources believed to be reliable. No guarantee is made to the completeness or accuracy of this information. Providence Capital Advisors, LLC shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions contained herein or their use, which do not constitute investment advice, are provided as of the date written, are provided solely for informational purposes, and therefore are not an offer to buy or sell a security. This information has not been tailored to suit any individual.

Providence Capital Advisors, LLC does not guarantee the results of its advice or recommendations, or that the objectives of a strategy will be achieved. Portfolios offered by Providence Capital Advisors, LLC may not have contained and/or may not currently contain the same underlying holdings and may have been and/or may currently be managed according to rules or restrictions established by Providence Capital Advisors, LLC. The income numbers for Covered Call and Diversified Income are based on one portfolio in the composite that serves as the model portfolio. Actual income returns may be different for other portfolios. Employees of Providence Capital Advisors, LLC may have holdings in the securities and/or utilize the same portfolio strategies as presented herein.

Benchmark returns are used for comparative purposes only and are not intended to directly parallel the risk or investment style of the accounts included in our investments. The volatility of the indices compared herein may be materially different from that of the compared Providence Capital Advisors, LLC strategy. There is no guarantee that the strategies will outperform, or even match, benchmark returns over the long term.

This commentary contains certain forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason.

Past performance is not indicative of future results. Therefore, no current or prospective client should assume that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended or undertaken by Providence Capital Advisors, LLC) will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client or prospective client’s investment portfolio. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the payment of which would have the effect of decreasing historical performance results.