19 May September 2020 – Driven by Few

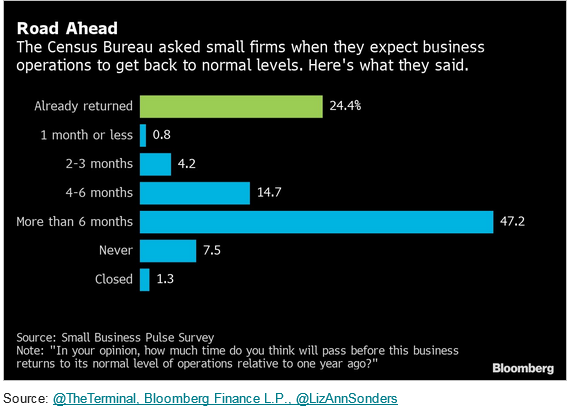

The stock market rebound that began this spring has continued its strength into the summer. This may seem incongruous against a backdrop of high unemployment, low consumer confidence, and a fragile recovery. The August survey below captures the difficulty felt by small business owners.

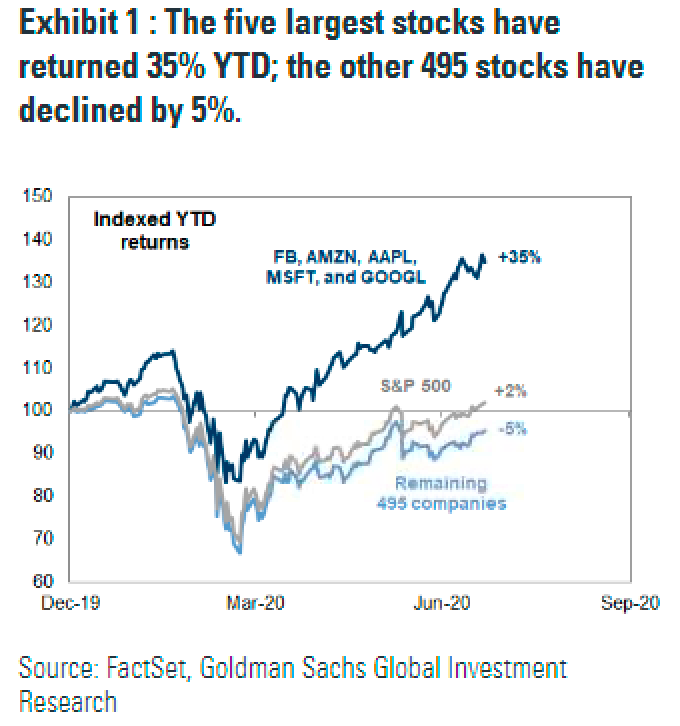

One way to explain the dichotomy between the economy and financial markets is that investing is forward-looking, and investors expect the economy to land on good footing once the COVID-19 pandemic is behind us. In our last newsletter I discussed the massive fiscal and monetary policy response to the economic contraction which was crucial in placing a floor under markets. Also in that newsletter, I mentioned that strong companies will not only survive, they will thrive during this pandemic. COVID-19 provided the perfect backdrop for technology companies as work, school, shopping, and socializing all shifted online. Success of the 5 largest companies in the S&P 500: Apple, Microsoft, Amazon, Alphabet (parent company of Google), and Facebook is masking difficulties at other companies and driving the return of the market. Data from Bloomberg shows that although the market is at a 52-week high, only 6% of stocks in the S&P 500 index are at 52-week highs. This narrow success is translating into a significant lack of breadth as the 5 aforementioned companies collectively make up about 24% of the S&P 500, eclipsing the last peak of concentration when the largest 5 companies made up about 18% of the S&P 500 during the late 1990s. The two charts below are from late July, and the gap widened further in August.

One segment of the market left behind by this technology surge is dividend paying stocks. Amazon, Alphabet, and Facebook do not pay dividends, while Apple and Microsoft both have a dividend yield below 1%. Clearly none of these stocks offer a high income stream for investors. There are a handful of different indices that track high dividend paying stocks, and year to date this segment of the market is down double digits and lagging the S&P 500 by about 25 percentage points. While it is impossible to call the timing of a rotation from one investment theme to the other, I do think market leadership could shift away from large technology stocks, and high dividend paying stocks are one potential future market leader. Interest rates are likely to stay low for the foreseeable future, and investors that cannot get enough income from bonds may need to own more high dividend paying stocks.

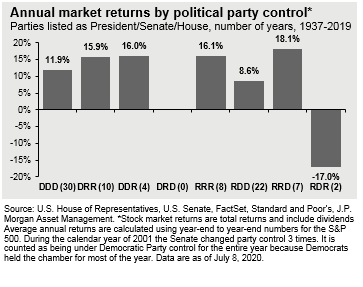

As we move into the fall, election rhetoric will heat up, and unfortunately much of this rhetoric will be targeted at people’s fears. Humans are wired to hate losses. In fact, according to studies referenced in the book, Nudge by Thaler and Sunstein, “losing something makes you twice as miserable as gaining the same thing makes you happy.” Fear is a powerful feeling that has helped humans avoid extinction since our first ancestors. I wish I could say the goal of the news media is to provide factual and unbiased information, but the true goal is to sell advertising by drawing eyeballs and clicks, and the current structure of our news media grabs eyeballs and clicks by latching on to people’s reactions to fear. This is important to remember as the media-driven fear increases over the next two months as we draw closer to the election. The chart below shows historic market returns under different Presidential, Senate, and House combinations. Throughout history the market has navigated most political backdrops fairly well.

Although the markets certainly could continue to grind upward, I think the highest probability is that we will see more volatility over the coming months. So with an expectation of increased volatility against a backdrop of fear-inducing news media, a few things to keep in mind this fall:

- We have raised cash across our investment portfolios to allow us to be opportunistic during times of volatility.

- It is impossible to eliminate risks in investing. Investors must accept risks to earn a return.

- It is impossible to time the markets. For example, missing just the best 5 days in 2020 would result in a year to date loss of about 25%. And all of those 5 days were in late March and early April when the economic backdrop looked horrible.

Lastly, I want to briefly mention the interesting human nature of hindsight bias. A timely article was published in The Wall Street Journal in late March, one day before the market bottomed. This article describes the general human tendency to reconstruct our feelings and actions from the past with less than complete accuracy once we know the actual outcomes. According to the article, “That intuition keeps you from learnings from mistakes, leads you to pay too much attention to unreliable forecasts, and makes you mismeasure your tolerance for risk.” This concept is another interesting point to keep in mind during the next market pullback, which invariably will occur.

Tom Searson, CFA